TL;DR: For most non-resident Estonian OU owners in 2026, open Wise Business first: it is remote, gives you a SEPA EUR IBAN, and accepts e-resident companies. Add Payoneer if your income comes from marketplaces, or a second EMI (Airwallex, Intergiro) for redundancy. A real Estonian bank account (LHV) is only realistic if you have genuine Estonian ties and can travel to Estonia once to identify yourself in person. The traditional Baltic incumbents (Swedbank, SEB, Luminor) are effectively closed to pure non-residents. Note on the IBAN: Wise does not give you an Estonian EE-IBAN; it issues a Belgian BE-IBAN, which is fully SEPA-valid and accepted everywhere in the EU.

Which banks actually accept a non-resident Estonian OU in 2026?

Wise, Payoneer, Airwallex and Intergiro accept non-resident e-resident OUs and onboard fully online. Among traditional Estonian banks, only LHV realistically opens accounts for e-residents, and only with a demonstrable connection to Estonia plus an in-person identification visit. Swedbank, SEB and Luminor almost never accept a pure non-resident.

The single most useful thing to understand: the account you can open remotely (Wise, Payoneer) is an electronic money institution, not a bank, and it does not give you an Estonian IBAN. The account with a real Estonian EE-IBAN (LHV) is a bank, and it will not onboard you remotely. You pick based on which of those two facts matters more for your business.

Bank-by-bank comparison

Real, sourced facts. "Accepts non-resident OU" means a company owned by someone who does not live in Estonia and holds only e-Residency, not an Estonian residence permit.

| Provider | Accepts non-resident OU? | EUR IBAN / SEPA | In-person visit? | Best for |

|---|---|---|---|---|

| Wise Business | Yes | Belgian BE-IBAN, full SEPA | No, fully remote | Default operating account for most non-residents |

| Payoneer | Yes (receiving) | EUR receiving account with IBAN/BIC, SEPA in | No, fully remote | Marketplace and platform income (Upwork, Fiverr, Amazon) |

| Airwallex | Yes | Multi-currency incl. EUR, SEPA | No, fully remote | Redundancy and APAC-facing businesses |

| Intergiro | Yes | EUR IBAN, SEPA | No, fully remote | Listed by e-Residency as a fintech alternative to Wise |

| LHV | Only with real Estonian ties | Estonian EE-IBAN, SEPA, deposit insured | Yes, one-time in Estonia | Established OUs with genuine substance and invoices |

| Swedbank / SEB / Luminor | Almost never | EE-IBAN (if approved) | Yes | Skip unless you actually live in Estonia |

Sources for the load-bearing claims: the official e-Residency business banking page names Wise, Intergiro and LHV and states that in-person visits are needed for Estonian banks but not fintechs; LHV's non-residents page states e-resident status alone is not sufficient and that you must come to an LHV office to identify yourself; Wise's own docs confirm the EUR account is a Belgian BE-IBAN (Wise Europe SA, BIC TRWIBEB1); Payoneer confirms EUR receiving accounts with local IBAN and no travel requirement.

Gap we could not close: real onboarding screenshots (the Wise KYB business-description screen, the LHV branch identification step) would materially strengthen this page. We do not have consented captures of those flows, so they are omitted rather than faked.

Who is the realistic winner for most non-residents?

Wise Business. It is remote, fast, accepts e-resident OUs, and its EUR account carries a real Belgian BE-IBAN that works for every SEPA transfer in the EU. For a location-independent founder invoicing clients directly, this is the correct first account and usually the only one you strictly need.

Who Wise is NOT for: anyone who needs deposit insurance on large balances (Wise safeguards funds rather than insuring them, so do not park reserves there), and anyone whose bank or client contractually requires an Estonian EE-IBAN. Wise's IBAN is Belgian, which is legally fine for SEPA but occasionally trips up a counterparty that expects an EE prefix.

When should you use Payoneer instead?

Use Payoneer when most of your revenue arrives through marketplaces and platforms rather than direct client invoices. Payoneer gives you an EUR receiving account with a local IBAN and integrates with thousands of marketplaces, and it opens fully online with no travel to Estonia required. It is a receiving layer, not full business banking.

Who Payoneer is NOT for: running your day-to-day outflows, paying suppliers, or acting as your only account. Pair it with Wise. Treat Payoneer as the pipe that collects platform income, then move operating cash to Wise for spending and transfers.

When is a real Estonian bank (LHV) worth it?

LHV is worth pursuing only once you have genuine Estonian ties and real trading history. LHV explicitly states that e-Residency status by itself is not a sufficient basis to open an account, that your company must show a clear connection to Estonia and a need to bank there, and that non-residents must come to an LHV office in person to be identified. After that first visit you can sign future agreements digitally with your e-resident ID.

The payoff is a real Estonian EE-IBAN, deposit insurance, and a bank that no counterparty will second-guess. The cost, per LHV's published figures, is roughly EUR 100 to 600 to open and EUR 10 to 60 monthly depending on category, plus the travel. Apply once you have six to twelve months of invoices, an Estonian accountant, and a clear rationale for incorporating in Estonia, not before. If a bank is already asking "where is your business really run from," expect the tax authorities to ask the same, which is the permanent establishment trap worth understanding before you lean into Estonian substance.

Why do Swedbank, SEB and Luminor reject non-residents?

Because their compliance appetite for non-resident customers without Estonian ties is near zero after the Baltic AML enforcement wave around 2018 to 2020. This is category-level policy, not a judgment of your specific business. You can apply, but a pure non-resident e-resident with no Estonian address, staff, or local customers is almost always declined.

Do not spend weeks on it. If you have been declined by a traditional bank, that outcome is expected, not a signal that something is wrong with you; our breakdown of why business bank applications get rejected covers the actual triggers and how to phrase around them.

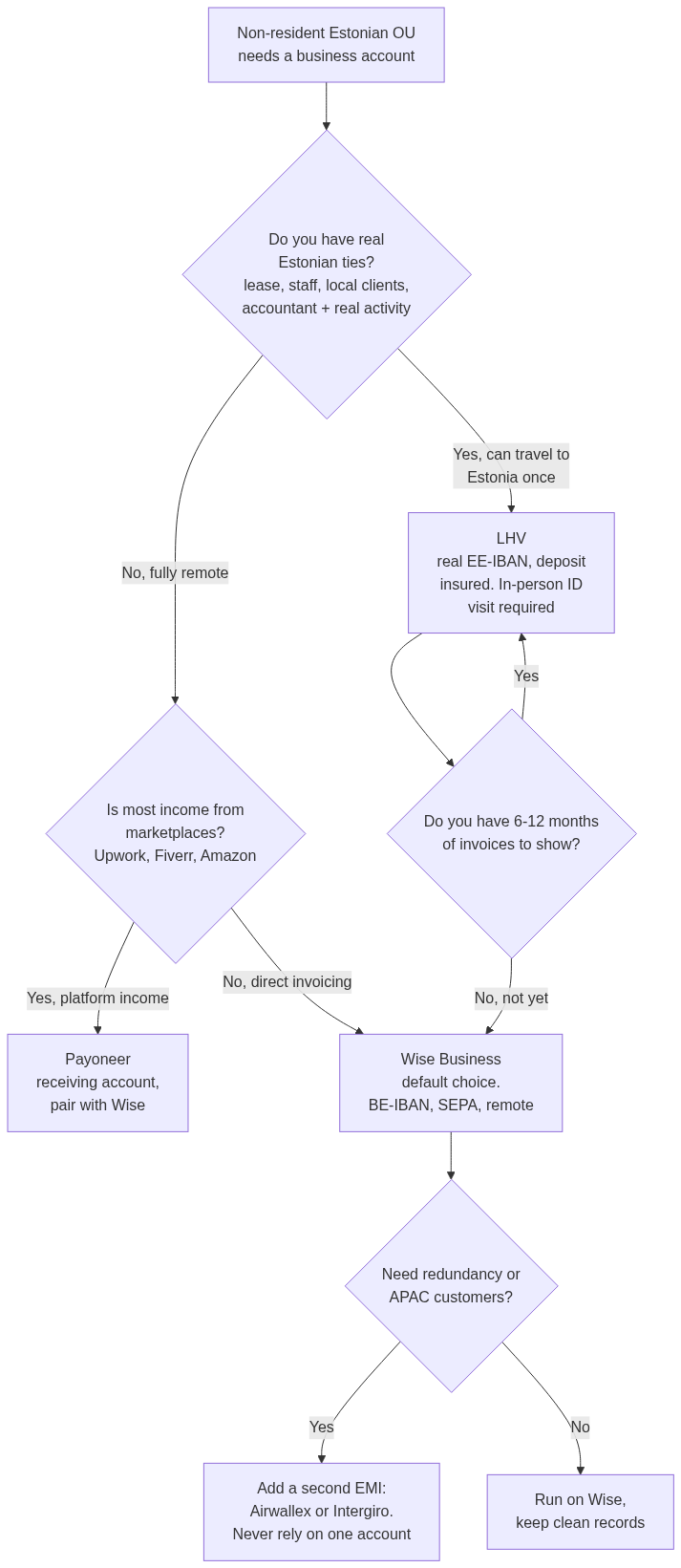

Which account fits your profile?

Use this decision flow. It front-loads the one question that actually decides the answer: do you have real Estonian ties, or are you fully remote?

The short version: fully remote and invoicing directly goes to Wise; marketplace income adds Payoneer; APAC or redundancy needs add Airwallex or Intergiro; and only genuine Estonian ties plus a stack of invoices justify the LHV route.

How to not get your fintech account declined or frozen

The two failure modes are a vague application at signup and an unanswered documentation request during a later review. Both are avoidable.

Be specific in the business description. "Consulting" gets flagged; "B2B technical consulting for European SaaS clients, billed monthly via Stripe and bank transfer, expected volume 5,000 to 15,000 EUR per month" gets approved. Keep your stated country of residence consistent with your address on file and your actual tax residency. And never run on a single account: open a second one early, because the most dangerous moment is an EMI freezing your only account during a routine review while you scramble for invoices you should already have. Clean bookkeeping from day one is the cheapest insurance you can buy, and it feeds directly into the true annual cost of running an OU.

FAQ

Can I open an Estonian bank account fully remotely as an e-resident?

You can open a fintech account (Wise, Payoneer, Airwallex, Intergiro) fully remotely. A real Estonian bank account at LHV requires a one-time in-person visit to an LHV office in Estonia to identify yourself; only after that can you sign further agreements digitally with your e-resident ID.

Does Wise give me an Estonian IBAN?

No. Wise issues a Belgian BE-IBAN through Wise Europe SA (BIC TRWIBEB1). It is fully SEPA-valid and accepted across the EU, but it is not an Estonian EE-IBAN. If a client or authority specifically requires an EE prefix, you need LHV, not Wise.

Is Wise a bank?

No. Wise is an electronic money institution authorised under the UK Electronic Money Regulations 2011. Funds are safeguarded in segregated accounts rather than covered by deposit insurance. For operational use this is fine; for parking large reserves, use a deposit-insured bank.

Do I need an Estonian bank to keep my OU in good standing?

No. The Estonian Commercial Register and Tax Board do not require you to bank in Estonia. You need a business account somewhere that can send and receive payments and accept the share capital contribution; a Wise Business account satisfies this.

What if every fintech declines me?

Apply to Wise, Airwallex and Intergiro in parallel and review your business description for vagueness. Persistent declines usually trace to a high-risk industry, a sanctioned-adjacent country of residence, or an application that reads like a shell company. Fix the description before reapplying.

Can my OU use my personal Wise or Revolut account?

No. You need a business account in the company's name. Mixing personal and business banking is an accounting and compliance problem and can undermine the limited liability of the OU. Before committing to the structure at all, it is worth checking whether an Estonian OU is even right for you.

This is general information, not financial or legal advice. Provider terms, fees and onboarding rules change often; confirm the current requirements with each provider before you apply.

Setting up your OU?

We can advise on which banking option is most likely to work for your specific residency and revenue profile, and how to phrase the application so it clears review the first time.